This article is more than

2 year old

Apple AAPL 0.32%increase; green up pointing triangle is pulling the plug on its credit-card partnership with Goldman Sachs GS -0.02%decrease; red down pointing triangle, the final nail in the coffin of the Wall Street bank’s bid to expand into consumer lending.

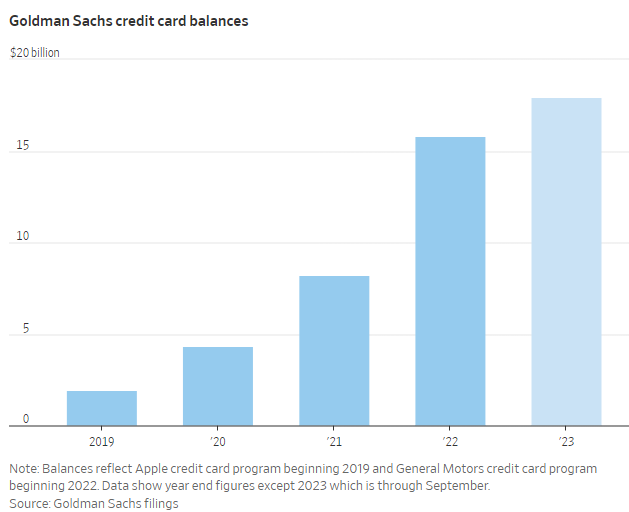

The tech giant recently sent a proposal to Goldman to exit from the contract in the next roughly 12 to 15 months, according to people briefed on the matter. The exit would cover their entire consumer partnership, including the credit card the companies launched in 2019 and the savings account rolled out this year.

It couldn’t be learned whether Apple has already lined up a new issuer for the card.

The move would mark a swift about-face for a program that just over a year ago was extended through 2029 and was intended to serve as a pillar of Goldman’s main-street ambitions.

The retreat began around the end of last year after Goldman lost billions of dollars trying to build out a full-service consumer operation.

By early this year, Goldman had told Apple that it would be looking to offload the partnership. Typically the merchant—in this case Apple—plays a controlling role in such partnerships.

Goldman has discussed with American Express the possibility of handing over the program to the card giant. Amex expressed concern about several aspects of the program, including its loss rates, and it isn’t clear if those discussions have continued.

Synchrony Financial has also been looking into the possibility of taking over the credit-card program, some of the people said. Synchrony, the largest issuer of store credit cards in the U.S., lends to a wide spectrum of consumers, including those with lower credit scores. Synchrony, which originally bid against Goldman for the Apple credit-card program, for years has been trying to position itself as an issuer with close ties to tech companies and counts Amazon and PayPal among its largest card partners.For Apple, the development is a setback for its services business, which the company has increasingly relied on as iPhone sales begin to slow—though to be sure, the Goldman partnership likely represents a small portion of that revenue stream. In Apple’s September quarter, overall sales were down less than 1% annually while services revenue advanced about 16%.

For Goldman, the partnership was a big part of its failed bid to diversify beyond businesses serving big corporate and investor clients and the ultrarich, and its demise is the final big step back from the failed experiment. Goldman is now turning back to focusing on those core clients.

The firm in November told employees it planned to end its other credit-card partnership, with General Motors, The Wall Street Journal previously reported. (GM is expected to run the process of finding a new issuer.) Goldman agreed in October to sell GreenSky, which specializes in making home-improvement loans, to a group of investors. It has stopped originating personal loans and sold off most of those balances.

Goldman and Apple’s relationship got off to a rocky start. Apple ran ads saying that the card wasn’t from a bank, irritating certain Goldman executives. Apple has pushed for nearly all applicants to get approved, pushing up loan losses for Goldman.

Apple has also insisted that cardholders get their bill at the beginning of the month, which has inundated Goldman customer-service employees with cardholders’ calls. Most card programs send out cardholders’ bills on a rolling basis to avoid such chaos.

Privately, some Goldman executives blame Apple for regulatory scrutiny that the bank has come under. Goldman disclosed last year that the Consumer Financial Protection Bureau is investigating its “credit card account management practices,” including how the bank resolves billing errors and refunds cardholders.

The Federal Reserve has been probing Goldman’s broader consumer-lending business. Goldman has been moving employees from consumer lending to an internal effort named Project Blue that is tasked with fixing regulatory issues.

Goldman is trying to figure out how to retain credit-card employees until the Apple account moves.

The bank this month told employees who work on its credit-card partnerships that they would be eligible for pay equal to one year of their compensation if their jobs are eliminated. Goldman is extending that program for certain employees, including in legal and engineering, who work outside of the consumer-lending unit but whose primary focus is serving its needs.

Aaron Tilley contributed to this article.